11.3 Appreciate the role of sustainability value chains and its link to management accounting

Leanne Gaul

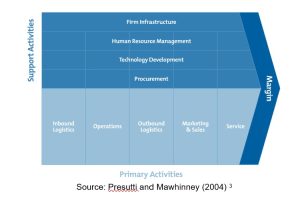

The concept of value is an implied promise by companies to deliver value to their customers.[1] Each measurement of unique value that can be delivered to a good or service is measured and contributed to the value chain.[2] The concept of value chains was developed by Michael Porter in 1985, which allows an organisation to map added value at each step of the production process from inbound logistics to operations, outbound logistics, marketing and sales, and finally service. The value chain also incorporates supporting activities of human resource management, technology, and procurement (see diagram below).

The value chain represents a set of progressive, interdependent activities depicted by linkages within the value chain. These interrelationships mean the value created by one activity bears a cost or impact to performance on another in the chain.[1] An additional insight is the corporate culture, found in the human resources practices of the support activities, which provides a basis to establishing a highly effective value chain.[2] All of the business activities detailed in Porter’s Value Chain provide opportunities for adding value to goods or services not only within the organisation’s operations but externally as well.

Given that organisations might be responsible for external costs that are not ordinarily acknowledged within traditional financial reporting methods as prescribed by accounting standards, the traditional value chain put forward by Porter (1985) might not sufficiently explain the true costs incurred and value contributed by organisations. To this extent, sustainability value chains have been developed to better capture these effects. The notion of sustainability considers the idea that business success and societal welfare must coexist.[3] This recognises an organisation’s need to embed TBL into their processes not only considering economic, environmental and social impacts of their operations from an internal perspective, but also impacts to the environment and society at large.[4] Some multinational firms have resorted to building their own value chains, incorporating sustainability related elements alongside the more traditional value chain categories described by Porter (1985). In essence, sustainability value chains attempt to show how organisational sustainability activities can lead to superior business outcomes.

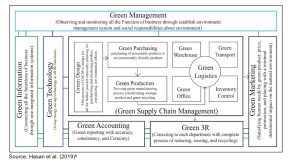

Hasan et al. (2019) developed a framework for a value chain incorporating support activities – Green Management, Green information, Green technology, Green Accounting, Green 3R – reduce, reuse and recycle – and Green marketing, which supports the supply chain – product/service design, purchasing, production and logistics, as depicted in the diagram below, providing interconnection of the value chain across the organisation from a sustainability perspective across all stages :

This value chain extends beyond traditional categories introduced by Porter above. The coloured lines demonstrate connectivity between activities of the organisation with green management, technology and information all feeding into accounting and each department through Green 3R.[5] Moving to the Green supply chain management (SCM) this is the process of producing the output, commencing with design. To complement the Green design, sustainable sources will be located in the Green purchasing portion of the SCM leading to Green production. The final part of the diagram Green Logistics is provided below:

[1] Presutti, W. D., & Mawhinney, J. (2013). Understanding the dynamics of the value chain (1st ed.). Business Expert Press. https://doi.org/10.4128/9781606494516

[2] ibid

[3] Presutti, W. D., & Mawhinney, J. (2013). Understanding the dynamics of the value chain (1st ed.). Business Expert Press. https://doi.org/10.4128/9781606494516

[4] ibid

[5] Hasan, M. M., Nekmahmud, M., Yajuan, L., & Patwary, M. A. (2019). Green business value chain: a systematic review. Sustainable Production and Consumption, 20, 326–339. https://doi.org/10.1016/j.spc.2019.08.003

[1] Bititci, U. S., Martinez, V., Albores, P., & Parung, J. (2004). Creating and managing value in collaborative networks. In D., Walters, & M. Rainbird (Eds.). (2004). Value chain. (251-268). Emerald Publishing Limited.

[2] ibid