Preparing a sales budget

Amanda White; Mitchell Franklin; Patty Graybeal; and Dixon Cooper

Why we need to prepare a sales budget

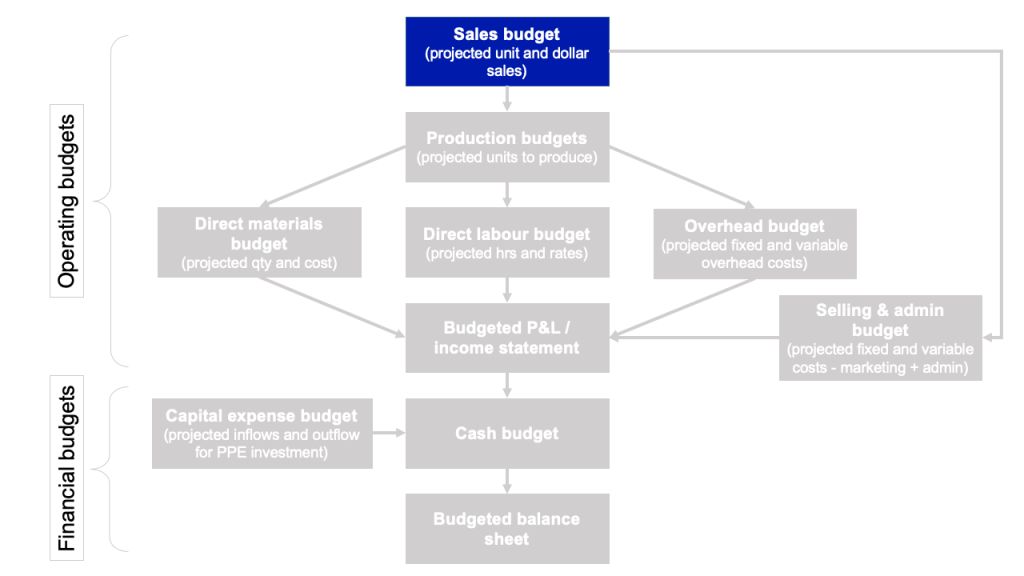

Remember that our operating budgets involve examining the expectations for the primary operations (sales and manufacturing of a good) of the business. Assumptions such as sales in units, sales price, manufacturing costs per unit, and direct material needed per unit involve a significant amount of time and input from various parts of the business. It is important to obtain all of the information, however, because the more accurate the information, the more accurate the resulting budget, and the more likely management is to effectively monitor and achieve its budget goals. In this section – we will start with the first part of our operating budget – the sales budget.

In order for a business to align the budget with the strategic plan, it must budget for the day-to-day operations of the business. This means the business must understand when and how many sales will occur, as well as what expenses are required to generate those sales. In short, each component – sales, production/manufacturing, and other expenses – must be properly budgeted to generate the operating budget components and the resulting budgeted P&L/income statement.

The budgeting process begins with the estimate of sales. When management has a solid estimate of sales for each quarter, month, week, or other relevant time period, they can determine how many units must be produced. From there, they determine the expenditures, such as direct materials necessary to produce the units. It is critical for the sales estimate to be accurate so that management knows how many units to produce. If the business under-estimates customer demand, they will not have enough inventory to satisfy customers, and they will not have ordered enough material or scheduled enough direct labour to manufacture more units. Customers may then shop somewhere else to meet their needs. Likewise, if sales are overestimated, management will have purchased more material than necessary and have a larger labor force than needed. This overestimate will cause management to have spent more cash than was necessary. No manager has a crystal ball and can predict demand precisely – but the better management and the marketing department can become at predicting demand, the businesses resources of materials, labour and cash can be most optimally utilised.

How to prepare a sales budget

The sales budget details the expected sales in units and the sales price for the budget period. The information from the sales budget is carried to several places in the master budget. It is used to determine how many units must be produced as well as when and how much cash will be collected from those sales.

The sales budget requires the business to generate a sales forecast for the year. The marketing department will work with management to build a sales forecast for the period (usually a year, broken down by quarters or months). That sales forecast will use the following information to generate sales:

- Sales activity for the business from previous years

- Competitor sales activity

- Industry trends

- Economy-wide trends

- Planned marketing campaigns

- Weather

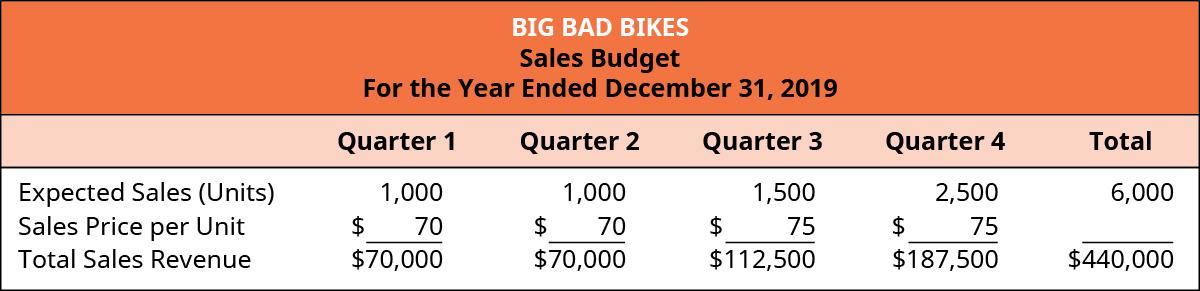

For example, Big Bad Bikes used the above information to estimate the number of units that will be sold in each quarter of the coming year. The number of units is multiplied by the sales price to determine the sales by quarter as shown in the table below.

The sales budget leads into the production budget to determine how many units must be produced each week, month, quarter, or year. It also leads into the cash receipts budget, which will be discussed in a later section.

Fluctuations in sales budgets

The expected sales units in the Big Bad Bikes example above shows that the new product is expected to increase sales in Quarter 3 and Quarter 4. This may be due to the fact that it will take time to build demand for this new product. It may also be because they expect greater sales towards Christmas.

Sales budgets for fruit and vegetable products may depend on the seasons. Sales budgets for livestock producers (such as beef, pork and lamb) will fluctuate in accordance with the reproductive schedules of animals, whereas for chickens it might be more standard. Sales budgets for seafood producers are highest in Australia around Easter (as Good Friday is a day where traditionally Christians eat seafood) and Christmas (where hot summers mean large turkey dinners that we see on television in the USA and Europe are not the normal). Butchers budget for almost non-existent sales of camel meat in Australia except around Ramadan, where camel burgers at night markets have become a common fixture at Ramadan night markets.

It is important to understand your business, your customers and your market when preparing a sales budget.